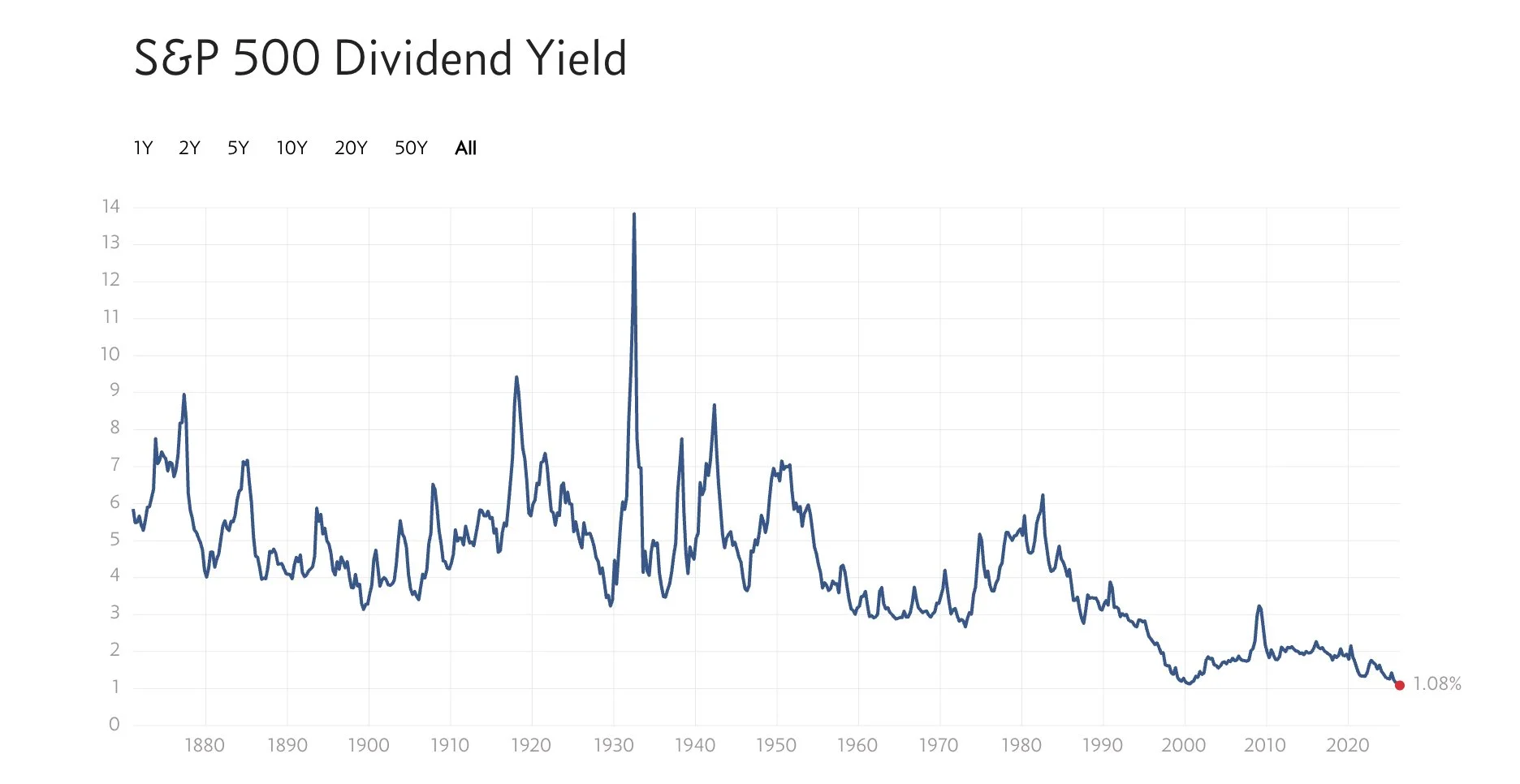

The S&P 500 has recorded a historic milestone as its dividend yield plummeted to 1.08%, the lowest level since the 1800s. This figure surpasses the previous low of 1.1%, observed at the turn of the millennium.

The Historical Context of S&P 500 Dividend Yields

Examining the S&P 500's dividend yield reveals a trend that emerged over decades. Typically, this yield offers insights into how companies distribute profits back to shareholders. A yield at just 1.08% indicates that investors are increasingly willing to sacrifice direct cash returns for potential capital gains. Historically, investors have expected higher yields during times of economic uncertainty or volatility. However, the current scenario suggests a different mindset. Many investors view stock price appreciation as more important than immediate cash flow. This shift may reflect broader trends in corporate behavior and investor expectations.

Negative Yields in Dividend Mutual Funds

There's a worrying development in the realm of dividend mutual funds: certain funds are reporting negative yields. This situation occurs when management fees and other expenses outpace the dividends these funds distribute. Investors who place their money in funds with elevated expense ratios may find themselves in a tough spot, as they effectively lose money on their investments, despite holding assets that traditionally provide returns through dividends. This raises questions about the sustainability of such funds in an environment that increasingly prioritizes discipline in fees.

Investors typically flock to dividend mutual funds for the stability they promise, but negative yields can erode the foundation of this strategy. If you’re working in this space, consider the implications: will your clients be willing to accept a negative return simply for the sake of owning dividend-generating assets? Given the historically low yields across the broader equity markets, shareholders may need to rethink their approaches to income generation.

A Shift from Dividends to Stock Buybacks

For some time now, stock buybacks have surpassed dividend payments as the favored method for returning capital to shareholders. Since the late 1990s, companies have increasingly opted to repurchase shares instead of distributing profits via dividends. Buybacks serve as a way to enhance earnings per share and can create immediate value for shareholders. Yet, this practice has sparked debate among investors regarding the long-term implications on corporate health and growth prospects.

Beyond the financial mechanics, this prevailing trend points to how corporations manage their capital. While stock buybacks can signal management's confidence in the company's future, they also pose risks. Over-leveraging to fund buybacks may lead to vulnerabilities during economic downturns. Moreover, many equity funds still emphasize dividends despite shrinking yields. This raises an interesting question: are investors underestimating the value available from buybacks and new share issuances? The answer has significant implications for how stock funds will have to adjust strategies in the ongoing competition for capital.

Warren Buffett’s Perspective on Shareholder Yield

Warren Buffett’s acknowledgment of shareholder yield over just focusing solely on dividends adds another layer of complexity. Over the years, he has continuously emphasized a holistic approach to returns, where share buybacks and management capital deployment are analyzed in conjunction with dividend payouts. His book, Shareholder Yield, remains a seminal read for those wishing to navigate these dynamics. Though initially published over a decade ago, the refreshed insights now available for free give new generations of investors a chance to reassess his approach amidst today’s changing landscape.

This perspective proves timely as investors digest insights from Berkshire Hathaway's latest meeting. With a hefty cash position of around $400 billion, Buffett’s comments underscore a prevailing preference within the company for stock buybacks instead of prioritizing dividends. It illustrates not just his strategy but also a potential trend among leading companies stuck with significant cash reserves. Investing this money through buybacks over paying dividends hints at future strategies that could redefine shareholder value metrics.

The Future Outlook: Will Yields Dip Below 1%?

As investors ponder the trajectory of dividend yields, the question arises: can we expect yields to slip below 1%? Given the current trajectory and the demand for growth over income, the odds appear steep. The market behavior suggests many investors are comfortable with low dividend returns as long as share prices continue to climb. This situation poses challenges for income-focused investors, who may find themselves squeezed further. Price dynamics and investor psychology will likely dictate the future of dividend yields.

Attaining yields under 1% might not be as shocking as it appears at first glance. If these trends persist, we’ll witness a fundamental reshaping of the frameworks used to evaluate stocks. Think about the implications here. Traditional views on corporation profit sharing might be upended, letting share buybacks take the main stage. As companies focus more on stock price appreciation, dividends may become a secondary concern for many. This could entirely redefine investor expectations regarding income generation.

Chart: Multpl