Recent research underscores the significance of dividend timing as a compelling factor influencing stock returns across 44 international equity markets. The study, leveraging data from 1993 to 2018, reveals that stocks that pay dividends consistently outperform non-dividend payers by around 0.58% per month, even when adjusting for global and regional risk factors.

Defining the Dividend Premium

The findings articulate a two-part structure to the dividend premium. One component relates to timing, driven by predictable investor behavior surrounding dividend events. Specifically, a notable trend exists where stocks experience heightened returns prior to ex-dividend dates, with a subsequent partial reversal afterward. The second component is persistent, manifesting outside of dividend event windows and linked to a stock’s governance and institutional quality.

Investor Demand Patterns

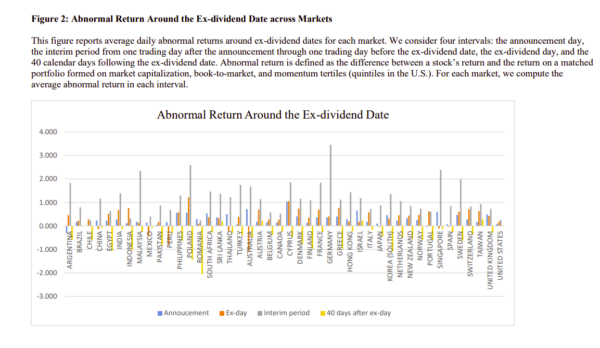

A key insight from the paper is that the demand for dividend stocks exhibits predictability. Historical data indicates that these stocks yield notably higher returns in months with expected dividend payments—1.47% during predicted ex-dividend months versus 0.94% in non-ex-dividend months. This gap widens to 1.01% during dividend months. The trend is also evident in daily data, which shows a price increase from the dividend announcement to the ex-dividend date, followed by a modest pullback, suggesting that dividend-seeking investors contribute to this price pressure.

Impact of Dividend Clustering

Dividend payout isn't uniformly distributed throughout the year; firms often cluster dividend payments due to fiscal conventions. For instance, nearly 60% of Japanese companies schedule their ex-dividend dates in March. The research finds that enhanced clustering correlates with a significant increase in the dividend premium. Specifically, a one-standard-deviation rise in clustering is linked to an additional 0.18% in the premium for the same month in the following year.

Global Synchronization of Dividend Premia

Interestingly, dividend premia are not merely localized phenomena. The study notes that markets sharing dividend calendars show greater co-movement in their dividend premia. When payout schedules align internationally, investor demand fluctuations impact multiple countries simultaneously. This interconnection suggests a potential rationale for global dividend factors that extends beyond mere macroeconomic variables.

Governance Factor

The research highlights that the persistent component of the dividend premium is especially pronounced in environments characterized by weak institutional frameworks. The premium is amplified in markets where liquidity is low, investor protections are inadequate, and regulatory frameworks are less stringent. In these scenarios, dividends serve as a trusted mechanism for distributing cash to shareholders.

Tax Implications

Conventional tax-based explanations for the dividend premium face limitations. The study indicates that the robust nature of dividend premium persists even in jurisdictions with similar taxation on dividends and capital gains—Hong Kong being a prime example. This complicates the argument that the premium is merely a response to tax considerations.

Insights for Investment Professionals

Understanding these dynamics presents actionable insights for investment advisors. Notably, the predictable nature of dividend-related returns around concentrated payout periods necessitates a nuanced approach to dividend investing, moving beyond yield as a singular focus. Recognizing and capitalizing on the seasonal effects of dividend demand can clarify short-term performance variances within equity markets.

Explaining to Clients

“Dividend-paying stocks generally outperform the market, not solely due to their dividends. Investors often show increased interest ahead of payout dates, substantially raising prices. When companies synchronize their dividend schedules, the resultant effect can ripple through entire markets. Moreover, dividends signal financial discipline, offering greater reassurance in markets where governance is less reliable.”

Visualizing the Findings

The results presented are hypothetical and do not indicate future outcomes or actual investor returns. Indexes mentioned are unmanaged and exclude trading fees, thus not directly investable.

Abstract Synopsis

This research across 44 international equity markets demonstrates a consistent dividend premium of 0.58% monthly when factoring in global and regional risks. This premium is segmented into timing and persistent components, with significant findings linking concentrated ex-dividend dates and weak institutional conditions to enhanced returns.

For further insights, refer to the full study published by Alpha Architect.